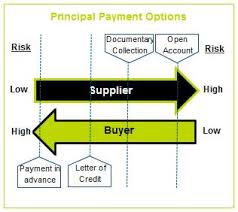

The best way to protect yourself as service providers, contractors or vendors against the risk of failure to receive payment upon delivery is to demand for some “Typical” Guarantee or Bond from BUYER. These guarantees and bonds are to be procured before delivery is made to the BUYER.

The execution of GUARANTEES or BONDS creates three parties as follows:

Buyer = Project owners (Primary Obligor)

Seller = Contractors, Vendors, Suppliers, exporter (Beneficiary)

Surety/Guarantor = Bank or Insurance Companies

These ”typical” Guarantees or Bonds are issued by the Surety/Guarantor at the request of the BUYER upon payment of Premium (%) of Contract Value.

The SELLER can demand for any of the financial guarantee and bonds listed below for protection the protection of their payment

(1) Deferred Payment Guarantee

(2) Letter of Credit (Inland or Foreign)

(3) Post Dated Cheques

(1) DEFEERED PAYMENT GUARANTEE

This is an assurance to the SELLER that BUYER will pay for goods supplied on a specific date. That is, BUYER will commit to a specific period in which all outstanding payment will be paid to beneficiary.

The maximum credit days (the specific date to pay) in DPG should be maintained at 90days

The seller offers credit to the buyer and buyer’s bank guarantees the due payments to the seller.

Perform = Payment

The Guarantee is issued by the Bank or Insurance company at request of BUYER in favour of SELLER

(2) LETTER OF CREDIT (LC)

Letter of Credit is a promise or commitment in writing made by a bank to a particular seller that payment will be made to the seller if the seller completes performing whatever is mentioned in the letter of credit. Payment here is not trigger by SPECIFIC DATE, payment is trigger once DELIVERY is made to BUYER. Letter of Credit is only used in foreign transactions. The type of Letter of Credit used for domestic transaction is called INLAND LC

LC is a form of Guarantee and is issued by the Bank or Insurance company at request of BUYER (local or foreign) in favour of SELLER

(3) POST DATED CHEQUES

Postdated cheque is one that is written with a future date indicated on it. This is usually done to account for an anticipated delay in deposit.

In Nigeria, like any ordinary cheques, post-dated cheques have a validity of 3 months from the date of issuance.

Post Dated Cheque is not a Guarantee issued by the Bank or Insurance company but rather an understanding between BUYER and SELLER to take advantage of illegal issuance of Post-Dated cheque without sufficient funds as a form of Guarantee for payment

*Knowledge shared here are for Sales and Marketing team of an organization or any individual assuming such a roles.